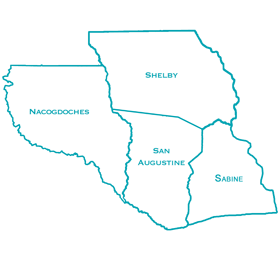

Membership is available to individuals who live or work in Nacogdoches, Shelby, San Augustine, or Sabine Counties. Becoming a member at Doches Credit Union is easy, and you'll find that you're more than just an account holder here — you're a member-owner! Think about it: Doches Credit Union truly is YOUR Credit Union.

Counties We Serve

Our History

Doches Credit Union is Nacogdoches’ only hometown not-for-profit financial cooperative that provides a full range of financial products and services to Nacogdoches, Shelby, San Augustine and Sabine Counties.

The Credit Union was chartered on November 7th, 1951, with an original field of membership comprised of employees from Southwestern Bell and the Lufkin Conroe Telephone Exchange.

In 1999, the Credit Union obtained a community charter which allowed services to be offered to any person that lived or worked in the Nacogdoches area as well as their families.

In 2005, Doches Credit Union opened its first full service branch in Center, Texas.

In 2011, its second full service branch opened across from Pilgrim’s Pride in Nacogdoches.

In 2013, Doches Credit Union completed a merger with Toledo Bend Teacher Credit Union, expanding the Credit Union’s reach into Sabine County.

Our Mission, Vision and Philosophy

Doches Credit Union’s mission is to empower our members and communities through the delivery of exceptional member service, innovative financial solutions, and personalized experiences which nurture economic well-being and provide long-lasting positive impact on the communities we proudly serve.

At Doches Credit Union, our vision is to be a premier financial institution, driven by the philosophy of “People Helping People,” known for exceptional member experiences, innovative solutions, and positive community impact.

We envision ourselves as being a trusted partner in our members’ financial journeys, delivering consistent value and excellence through the latest technology, industry best practices and continuous evolution to meet our members’ evolving needs. We envision that our comprehensive and accessible financial solutions will empower individuals, families, and businesses to achieve their goals and dreams, positioning us at the forefront of the financial services industry.

DCU’s philosophy begins and ends with understanding and meeting member needs. Member-owners are at the forefront of all decision made. As a result, DCU offers a full array of financial services including low-rate consumer loans , high-yield savings programs , systematic investments, free checking and debit options , and free online services .

For more than 60 years, Doches Credit Union has been an important contributor to the local economy. We remain dedicated to serving the communities in which we operate.

Our Core Values

Member-Centric Focus: We prioritize the needs and interests of our members above all else. Our decisions and actions are guided by a deep understanding of their financial goals, and we are committed to delivering exceptional service and tailored solutions to help them achieve success.

Trust and Integrity: We operate with unwavering integrity, maintaining the highest standards in all aspects of our operations. Trust is the foundation of our relationships, and we are committed to being transparent, honest, and accountable in every interaction.

Financial Education and Empowerment: We are passionate about financial education and empowerment. We strive to equip our members and our team-members with the knowledge, tools, and resources needed to make informed financial decisions and improve their financial well-being. We believe that by empowering individuals, we contribute to the overall economic growth and stability of our communities.

Community Engagement: We are deeply rooted in our communities and committed to making a positive impact. Through active community engagement, we support local organizations, initiatives, and causes that align with our values. We believe in building strong and vibrant communities where everyone has the opportunity to thrive.

Collaboration and Teamwork: We believe in the power of collaboration and teamwork. We foster an environment where team-members work together, share knowledge and expertise, and support each other to achieve common goals. By leveraging the collective strength of our team, we provide the best possible outcomes for our members.

Compliance and Ethical Conduct: We uphold a culture of compliance and ethical conduct. We are dedicated to adhering to all applicable laws, regulations, and industry standards to ensure the trust and confidence of our members and stakeholders. Our commitment to compliance guides our decisions and actions, allowing us to maintain the highest level of integrity in all aspects of our operations.

Your Board of Directors

Doches Credit Union operates under the governance of members elected to serve on the volunteer Board of Directors. The primary responsibilities of the volunteer Board of Directors include:

- Setting policies and planning for the future of DCU.

- Ensuring the sound financial condition of DCU.

- Reviewing the CEO's progress in achieving goals.

- Reporting to members at the annual meeting.

The Executive Staff plays a crucial role in bringing the Board of Directors' vision to life. They implement the vision by creating and executing a tactical plan to achieve the established goals.

| Freddie Gibson | Chair |

| Edeska Barnes | Vice Chair |

| Clara Bryant | Secretary |

| Selita Hoya | Treasurer |

| Saville Harris | Board Member |

| Daniel Johnson | Board Member |

| Joshua Moore | Board Member |

For inquiries regarding joining the Board of Directors, please reach out to us via email at [email protected].